Introduction to Wine Investing: How To Understand The State of the Overall Wine Market

To invest in anything, the very very very bare minimum knowledge threshold required is the value of what you’re buying, and how it has performed in the past.

In this edition of The Wine Investing Newsletter, I will be addressing the second point. How do we understand how wine has performed as an asset?

How do I measure how wine markets have performed?

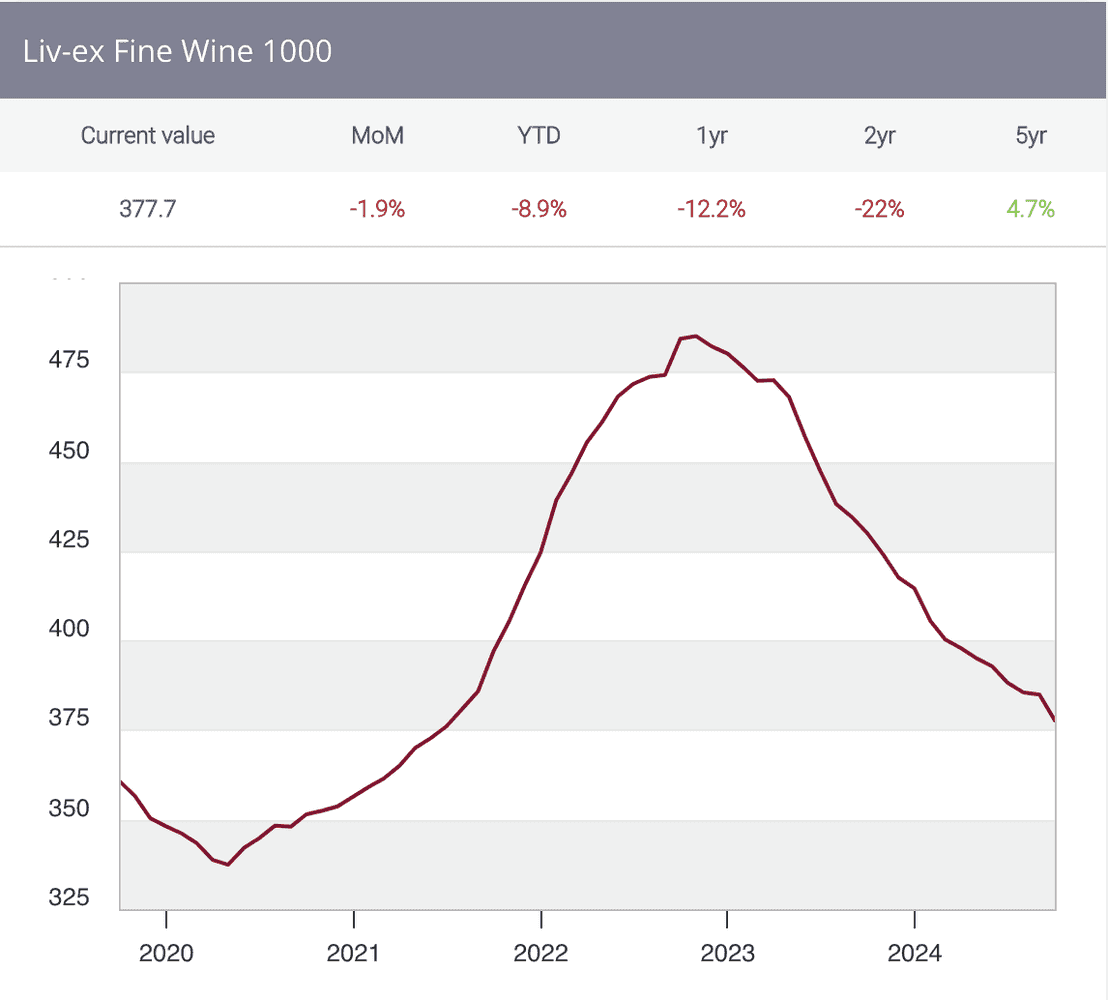

The Liv-ex

The industry benchmarks are typically the Liv-ex indices – in the same way traditional equities have the S&P500 and the FTSE100 etc..

The Liv-ex describe themselves as “the global exchange for the wine trade” – which is pretty much fair enough if you’re looking at ‘trade only’ exchanges. There are some other notable exchanges which are accessible by the general public.

If you’re thinking of investing in wine, then it’s likely that these indices will be one of the first places you go to understand what the market is doing.

For the uninitiated, the Liv-ex effectively act as a ‘stock market for wine’. Only trade members are allowed access and users can place bids and offers on different wines.

The Liv-ex publish a number of indices, the exact weighting / construction of which is not publicly available, but we can infer that they use the ‘mid price’ (more on that in a future newsletter), of the most traded (also one to dig into, value or volume?) wines on the market for each given bracket.

The Liv-ex 100 and 1000 are the ‘most traded’ 100 and 1000 wines on the market. The Bordeaux 500 are the 500 most traded wines from Bordeaux on the market and so on and so forth.

The Liv-ex 1000 “comprises seven sub-indices which represent the most traded wines from regions around the world: the Bordeaux 500, the Bordeaux Legends 40, the Burgundy 150, the Champagne 50, the Rhone 100, the Italy 100 and the Rest of the World 60.”

The Liv-ex 1000, taken from

The Liv-ex are rightly incentivised to provide the most efficient measure of the market. They want to provide investors price changes for the wines that are traded the most, because the prices of those wines are the most accurate.

The most highly traded wines however, are not necessarily the highest returning. The Liv-ex 100 and Liv-ex 1000 are both heavily weighted towards Bordeaux which has underperformed since 2011. For example, there are 540 Bordeaux vintages in the Liv-ex 1000

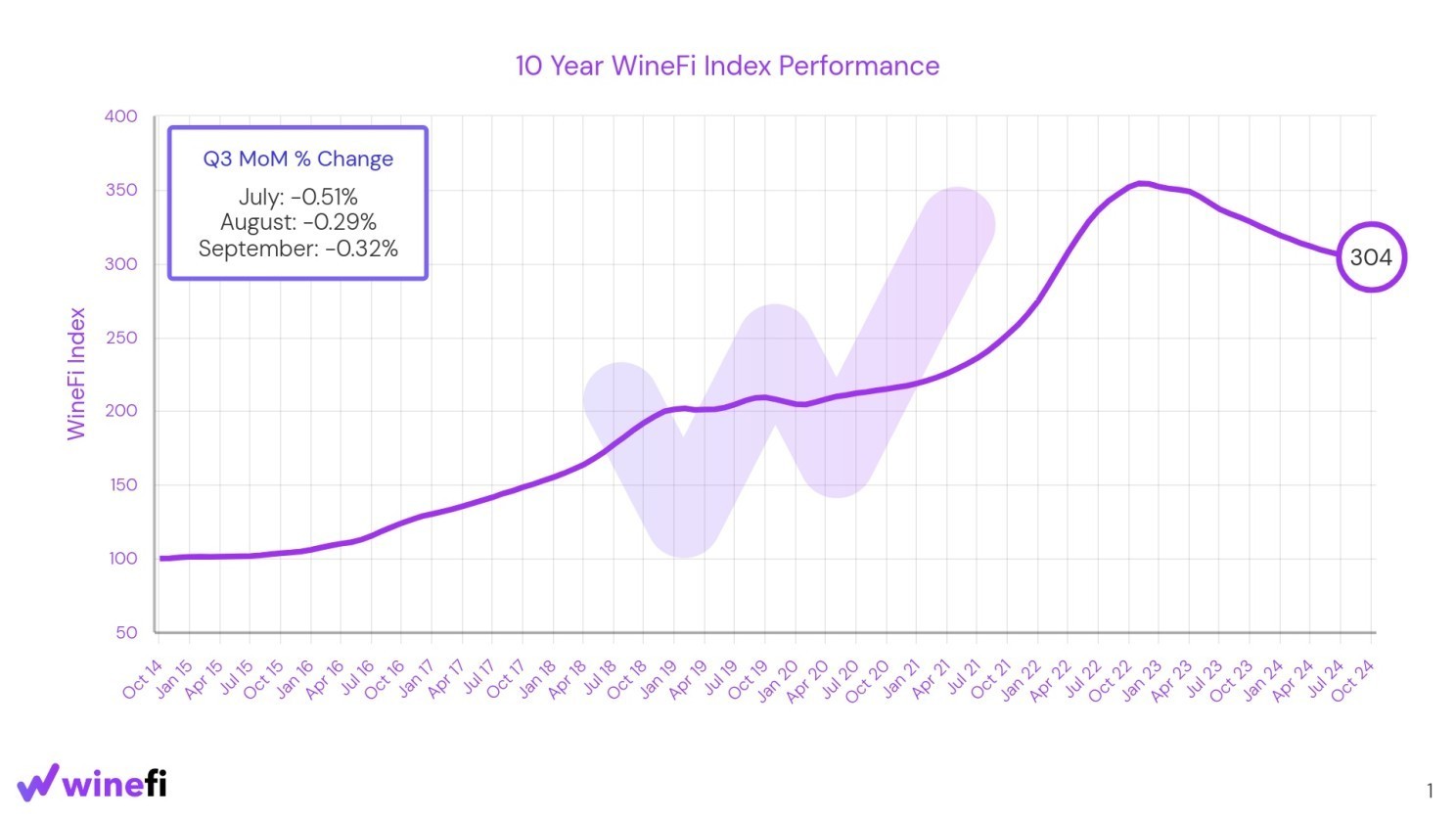

WineFi

At WineFi we are incentivised to identify the wines with the most potential to appreciate, and we want to include those wines in any market measuring that we do.

This translates to a broader approach when measuring the market.

We want to include every wine price that we can confirm is accurate. This means that we input as much data as possible, clean it (sorry Aaran Daniel) to make sure the prices are an accurate reflection, and translate it.

The WineFi Index therefore does not set an upper bounds on the number of wines that can be included. We instead set criteria that must be met for a wine to be included.

10 Year WineFi Index Performance

A wine qualifies if it:

Meets our minimum liquidity criteria; the label has sufficient current market depth based on visible offer depth at a trusted stock-holding merchant.

Is priced above £80/bottle or equivalent inflation-adjusted historical price.

is vintage 1968 or later

Regional weightings are based on Market Share by Trade Value according to the Liv-ex. The highest-priced wines are prioritised for selection in the index first. The indices are calculated on a price-weighted basis.

This means that wines with lower trade volume are included, and so we can capture a greater number of investment grade wines when measuring, and analysing market performance.

The idea is that the index will include wines that are less traded, but perform in a different manner to the Liv-ex indices. This allows us to identify regions, sub-regions, labels, and vintages that out(and under)-perform the markets.

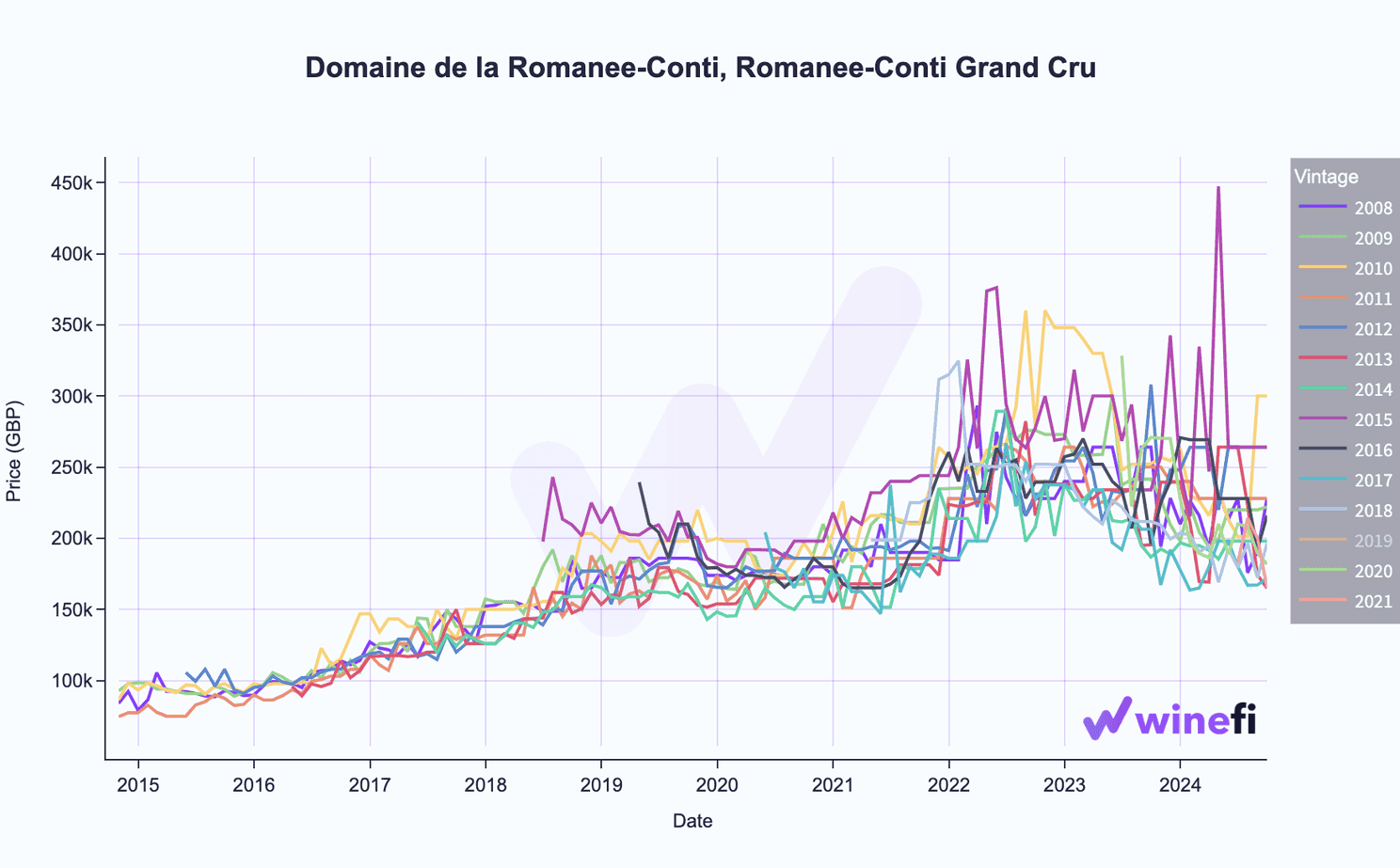

On a wine by wine level

At WineFi, we have tools to understand the characteristics of a specific vintage of a specific label over the last X period. See below for a behind the scenes look at AskAaran (named that way because Aaran, our Head of Data wanted us to stop bothering him for wine performance charts).

Ask Aaran – DRC Romanée Conti Vintage Performance

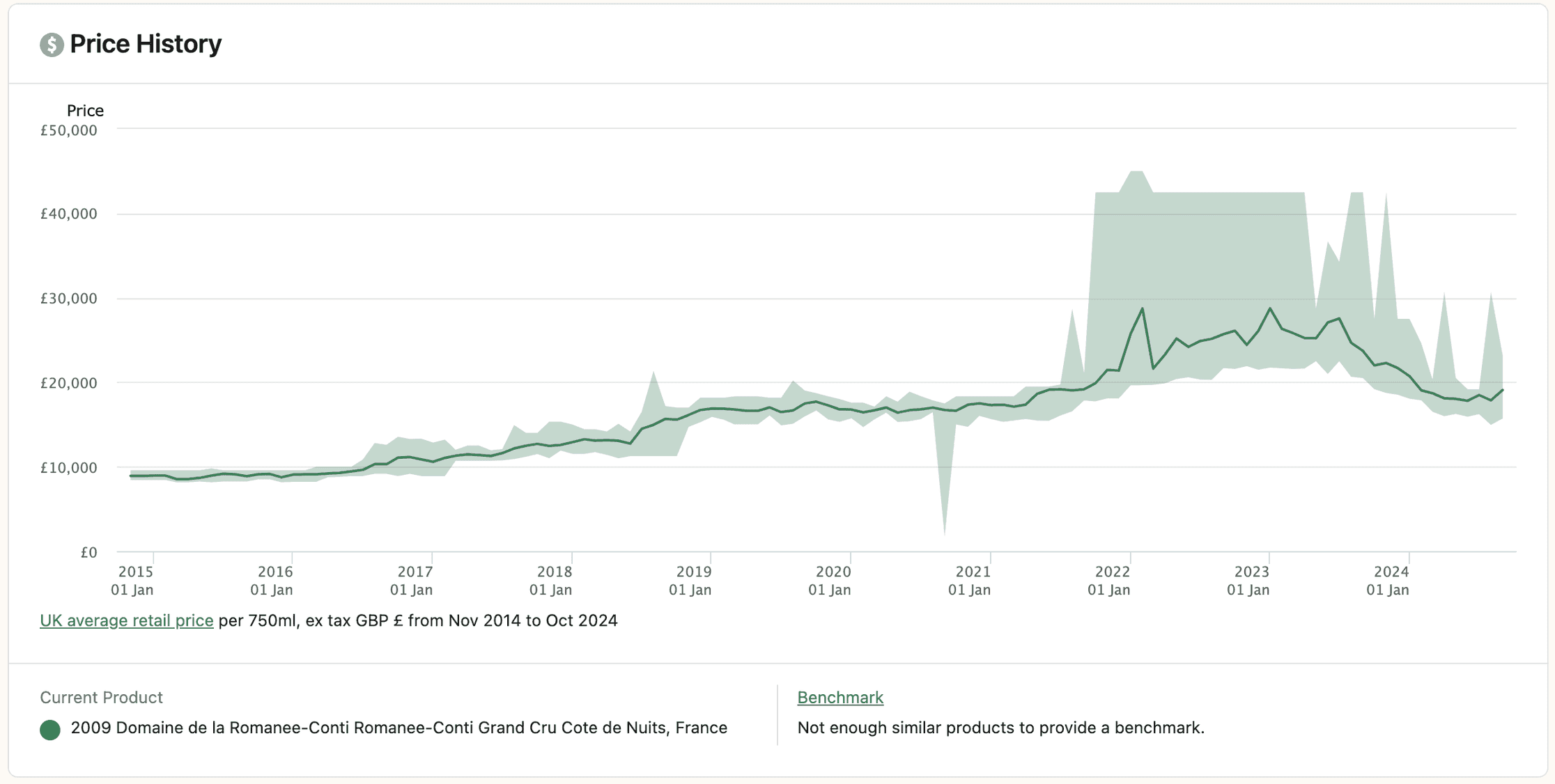

To someone getting started, WineSearcher is a good place to start. If you want to know how the 2009 DRC Romanée Conti has performed recently then the analytics page is a good place to go.

Credit to WineSearcher

There are a whole host of other metrics to look at when analysing on a wine by wine level, which will be the focus of a future newsletter.

Conclusion

All of the measures stated will give you a sense of how the wine markets are performing, and they will (likely) paint a similar picture.

The key distinction is that the Liv-ex indices will provide the most accurate snapshot of the most traded wines in the market. If you only plan to invest in the most traded wines then these will accurately reflect how your portfolio may have acted over the past year.

The WineFi indices provide a broader picture of how the markets are doing as a whole, but will include wines with less secondary market activity, and potentially less liquidity.

As a very basic piece of analysis – if the WineFi Index outperforms the Liv-ex 1000 (which it has over the past 10 years), then it is likely that the most-traded wines are not the ones that are outperforming the market, and vice versa.

If you’re thinking about investing in wine and you want to understand how the market is doing, both measures are important to get a proper grasp on market performance and to have the best idea you will likely want to take a look at both, and much more!

Capital is at risk. Wine values can go down as well as up, and investments may not perform as expected. Returns may vary. You should not invest more than you can afford to lose. WineFi is not authorised by the Financial Conduct Authority. Investments are not regulated and you will have no access to the Financial Services Compensation Scheme (FSCS) or the Financial Ombudsman Service (FOS). Past performance and forecasts are not reliable indicators of future results and should not be relied on. Forecasts are based on WineFi’s own internal calculations and opinions and may change. Investments are illiquid. Once invested, you are committed for the full term. Tax treatment depends on individual circumstances and may change.

You are advised to obtain appropriate tax or investment advice where necessary.

WineFi is a trading name of WineFi Management Limited. Registered in England and Wales with registration number: 14864655 and whose registered office is at 5th Floor, 167-169 Great Portland Street, London, United Kingdom, W1W 5PF.