Producer Spotlight: Cedric Bouchard

Investing in Cedric Bouchard

Overview

In the heart of the Côte des Bar, where Champagne tradition meets quiet audacity, Cédric Bouchard has reshaped the idea of grower Champagne. When he launched his own label in 2000, it was with just one inherited hectare, Les Ursules, and a vision to craft wines that express nothing but place and personality.

His philosophy is radical in its precision: single-vineyard, single-vintage, single-variety Champagnes, made at ultra-low yields, often only 20–30 hl/ha, less than half the regional average, and bottled with no dosage, no fining, and only natural yeasts.

The results are Champagnes of striking purity: powerful yet transparent, structured yet silken, finishing with a creamy texture that reflects Cédric’s deep affection for Burgundy.

Quick Facts - Cedric Bouchard, Roses de Jeanne Les Ursules Blanc de Noirs

Attribute | Details |

|---|---|

Region | Côte des Bar, Champagne, France |

Grape Varieties | Pinot Noir |

First Vintage | 2000 |

Critically Acclaimed Vintages | 2008, 2014, 2016, 2017, and 2018 |

Average Critic Score | 94.7 |

Current Market Liquidity | Scarce |

Drinking Window | 5 - 10 years. For 2017 (20 years) |

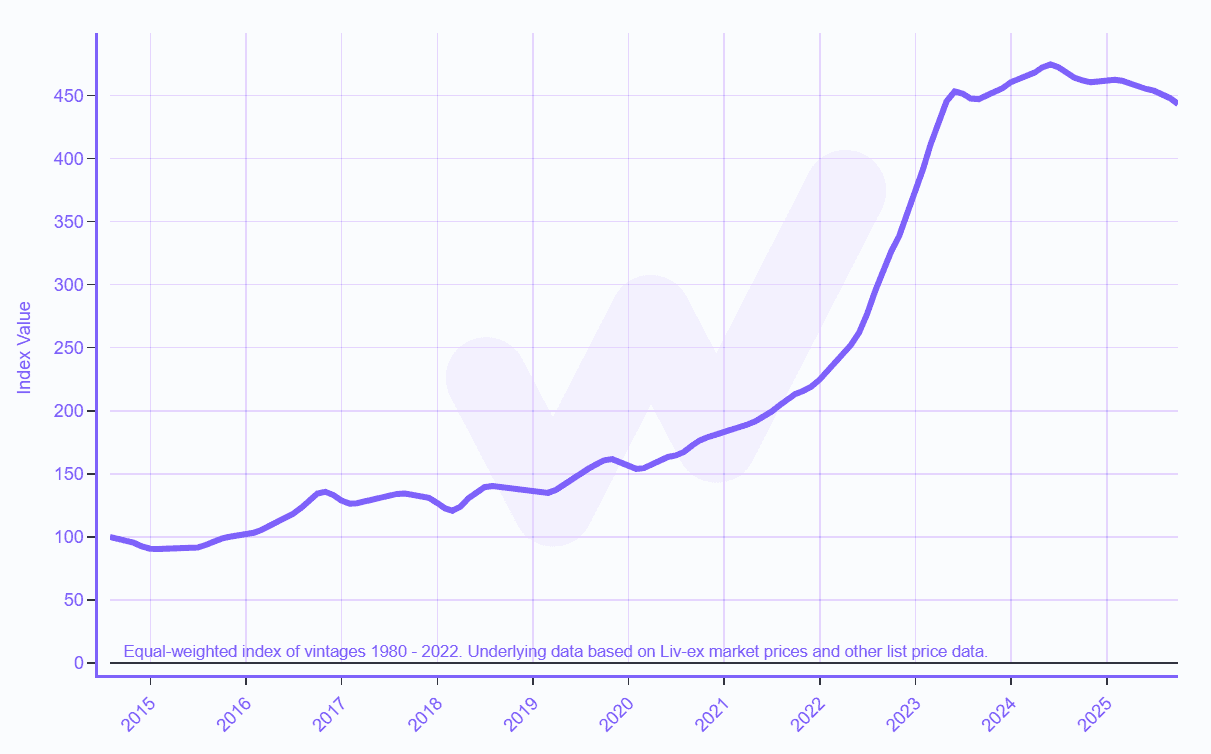

Cedric Bouchard, Roses de Jeanne Les Ursules Blanc de Noirs Label Index Tracker

Analyst Note - From Matthew Small (Head of Investment)

Les Ursules is the only Roses de Jeanne vineyard not owned by Cédric Bouchard. *Roses de Jeanne* being the name of his estate, chosen as a tribute to his grandmother Jeanne and her rose garden. Production is tiny, averaging just a few hundred bottles of the top selections each year.

The Bouchard Les Ursules index shows an average annual 10-year CAGR of 16%, alongside an average critic score of 95. This combination of consistently high scores, extremely limited production, and strong momentum in the grower Champagne market makes Cédric Bouchard’s Les Ursules one of the most compelling investment opportunities in fine wine today.

Dinner Party Story

When first presenting his wines to Parisian sommeliers, Bouchard insisted they be served in Burgundy glasses instead of flutes. His reasoning? These weren’t to be viewed as “Champagne” first, but as pure expressions of terroir. Some were shocked, others delighted—but in that moment, he reshaped how many thought about Champagne altogether.

Capital is at risk. Wine values can go down as well as up, and investments may not perform as expected. Returns may vary. You should not invest more than you can afford to lose. WineFi is not authorised by the Financial Conduct Authority. Investments are not regulated and you will have no access to the Financial Services Compensation Scheme (FSCS) or the Financial Ombudsman Service (FOS). Past performance and forecasts are not reliable indicators of future results and should not be relied on. Forecasts are based on WineFi’s own internal calculations and opinions and may change. Investments are illiquid. Once invested, you are committed for the full term. Tax treatment depends on individual circumstances and may change.

You are advised to obtain appropriate tax or investment advice where necessary.

WineFi is a trading name of WineFi Management Limited. Registered in England and Wales with registration number: 14864655 and whose registered office is at 5th Floor, 167-169 Great Portland Street, London, United Kingdom, W1W 5PF.