How will Interest Rate Cuts Affect the Wine Market?

Interest Rates and the Fine Wine Market

The Bank of England has cut interest rates for the first time since 2020 as inflation continues to remain steady, holding at their two percent target for two consecutive months.

Bank Rate has been moved from 5.25%, a 16-year high where it has been pegged for the last year to fight inflation, to 5% – a drop of 0.25 percentage points.

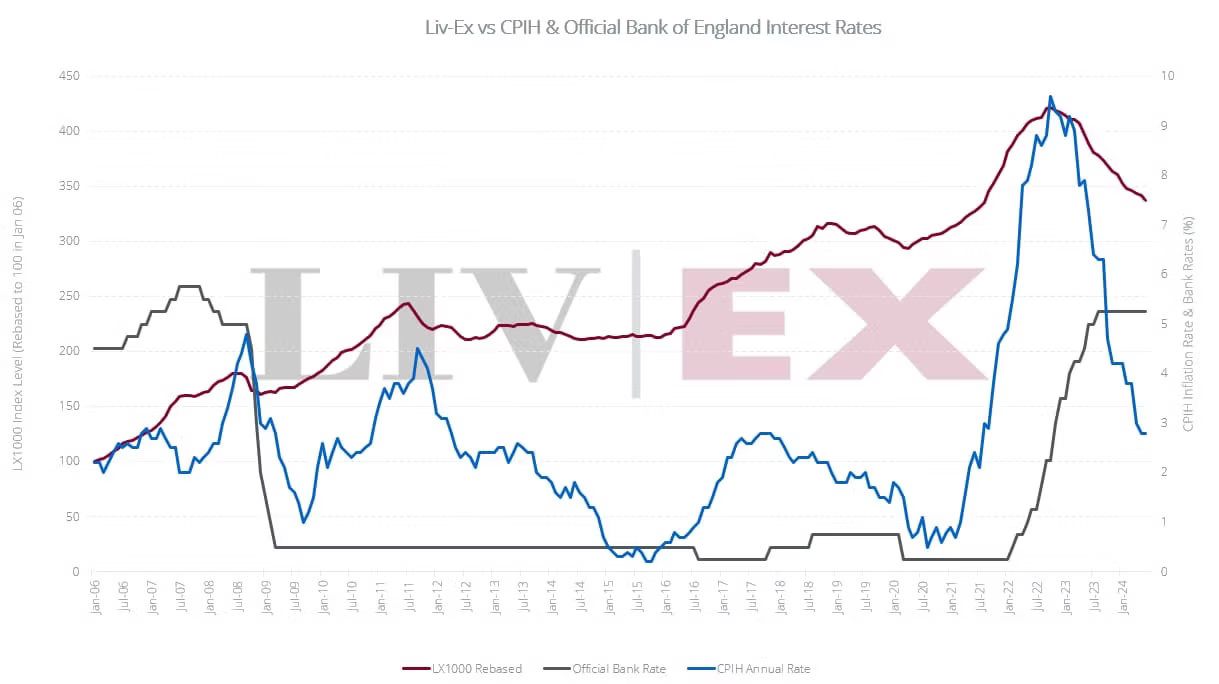

Wine prices, often regarded as both a luxury item and an investment, are influenced by interest rate changes through various channels. By examining the chart below (which displays the Liv-ex Fine Wine 1000, Bank of England interest rate, and the Consumer Prices Index (CPIH)), we can observe several instances where a drop in interest rates preceded a significant rise in the market – notably in early 2009, mid-2016, and early 2020.

These upward trends can largely be attributed to heightened demand from both consumers and investors. While a reduction in interest rates generally boosts the industry’s prospects, those looking to profit may anticipate certain indices to climb more rapidly than others. Additionally, buyers using Euros and Dollars stand to gain from the impact of rate cuts on exchange rates.

The market demand and interest rates dynamic is well documented. For instance, following the onset of Covid-19 in February 2020, the Bank of England reduced interest rates to stimulate economic growth. This led to a surge in spending across various sectors, including the wine industry. Increased disposable income, particularly during prosperous times, tends to boost demand for mid-range wines (£1,000–£2,000 per 12×75), making them accessible to a broader range of consumers.

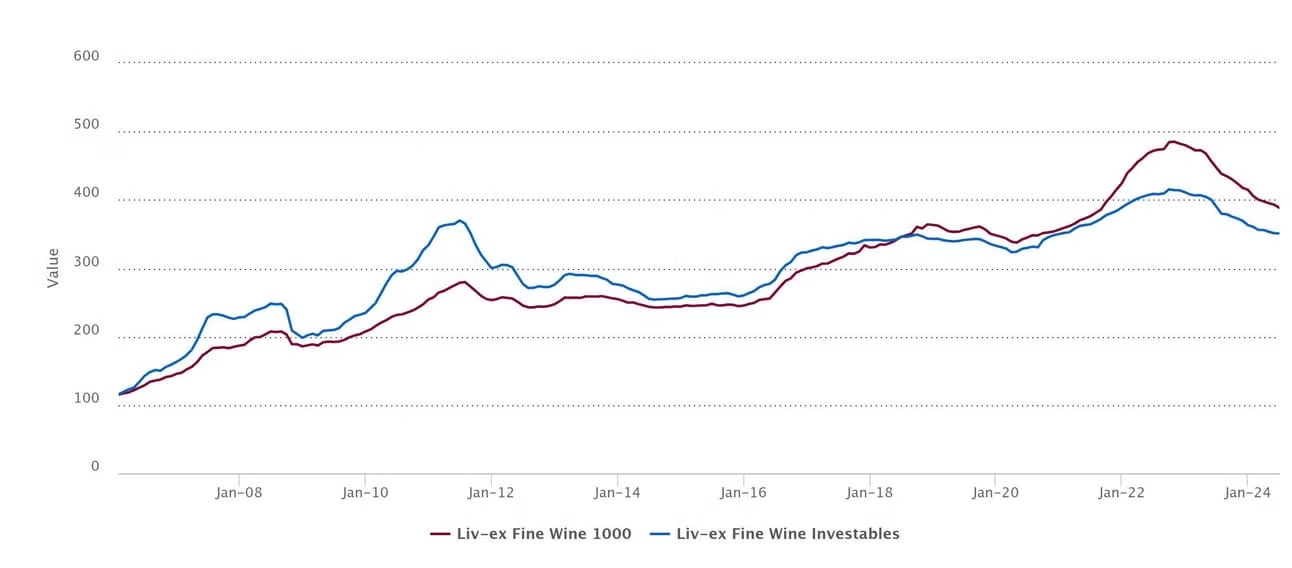

However – the world of wines that WineFi considers as ‘investment grade’ tends to be above this price bracket. The chart below illustrates the price trends of the Liv-ex Fine Wine 1000 and Liv-ex Investables index since 2006. The Investables index contains a basket of wines at a higher price point than the £1,000–£2,000 per 12×75 listed above.

During the inflationary period from early 2021 to mid-2022, the Investables index exhibited less price volatility compared to the 1000.

This suggests that prices of these wines are less influenced by spending tendencies and more by expectations of future returns, similar to stock prices. This idea is further supported by the sharp decline in the Investables index in August 2011, which coincided with the stock market crash. Buyers investing in wine tend to be motivated less by affordability and more by the perceived stability of the market.

Capital is at risk. Wine values can go down as well as up, and investments may not perform as expected. Returns may vary. You should not invest more than you can afford to lose. WineFi is not authorised by the Financial Conduct Authority. Investments are not regulated and you will have no access to the Financial Services Compensation Scheme (FSCS) or the Financial Ombudsman Service (FOS). Past performance and forecasts are not reliable indicators of future results and should not be relied on. Forecasts are based on WineFi’s own internal calculations and opinions and may change. Investments are illiquid. Once invested, you are committed for the full term. Tax treatment depends on individual circumstances and may change.

You are advised to obtain appropriate tax or investment advice where necessary.

WineFi is a trading name of WineFi Management Limited. Registered in England and Wales with registration number: 14864655 and whose registered office is at 5th Floor, 167-169 Great Portland Street, London, United Kingdom, W1W 5PF.