Investing in Fine Wine - An Introduction

Investing in Fine Wine: An Introduction, the Benefits, and the Issues

Introduction

Fine wine is a unique asset class for many reasons, and when approached correctly can yield attractive returns. However, knowing where to start is hard – there is a wealth of knowledge which remains inaccessible to most would-be investors.

The wine industry is very much an “old boy’s club” and the experience of investing in wine has often reflected that attitude.

It is no secret that wine investment is a specialist topic. Many investors who are otherwise knowledgeable about mainstream asset classes may know very little about wine. Unhelpfully, there is also a culture of “take our word for it” that permeates the wine investment landscape.

As a result, less knowledgeable investors sometimes end up with portfolios filled with wines that are unlikely to appreciate or for which there is no secondary market at all.

We are committed to making our analysis transparent, and providing investors with the tools to making an informed decision.

The Benefits

A unique supply/demand dynamic

The fine wine market is driven by supply and demand.

There are a limited number of “blue chip” producers across a handful of top wine regions.

Only a finite number of bottles can be produced by each winery every year, the quality of which varies from vintage to vintage.

As the wines improve with age and bottles are consumed or damaged, they become increasingly scarce. At the same time, as global wealth increases, so too does demand for high-end wine.

This combination of ever increasing scarcity and growing demand helps to drive prices higher.

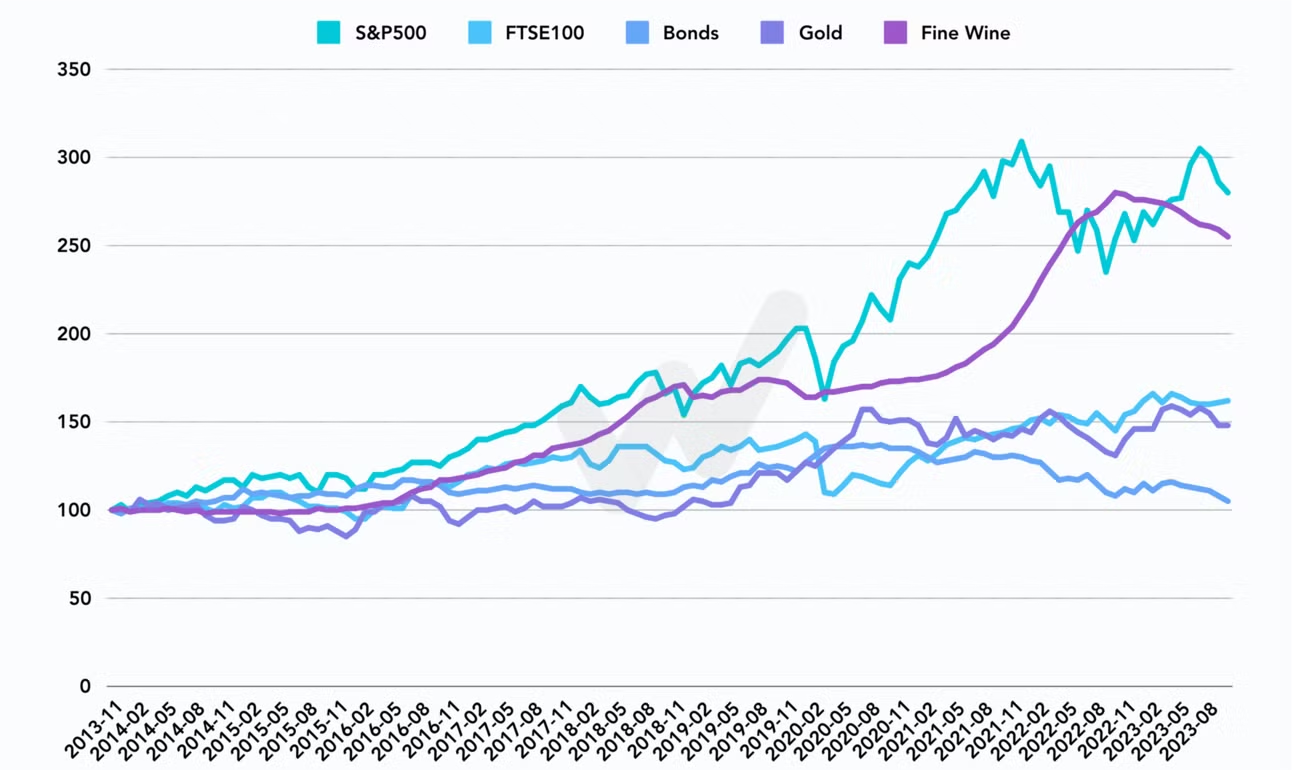

Performance

Fine wine, especially on a regional level, compares favourably to mainstream equity indices even when factoring in dividend reinvestment.

The graph below compares the long term performance of various mainstream asset classes compared to a price-weighted index of ~8000 frequently traded fine wines.

The wine market downturn in late 2023 / early 2024 has led to blue chip assets trading well below their all time highs, providing an attractive opportunity for new investors looking to access the asset class.

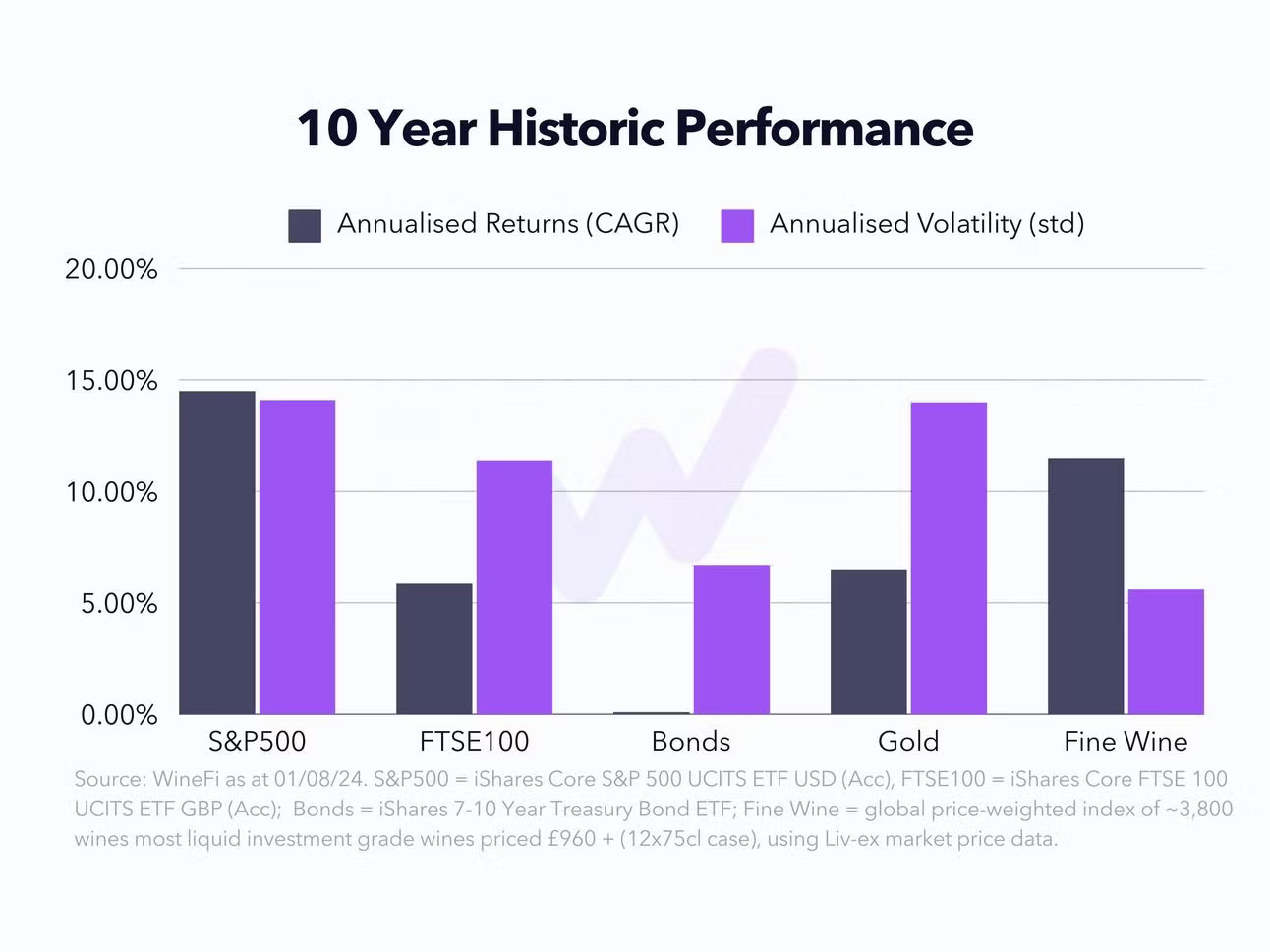

Volatility

As well as the market’s favourable supply-demand dynamic, wine’s volatility profile stems from a lower liquidity. Whilst this can be a drawback, it does mean that the asset class is protected from panic selling in the event of a broader economic downturn.

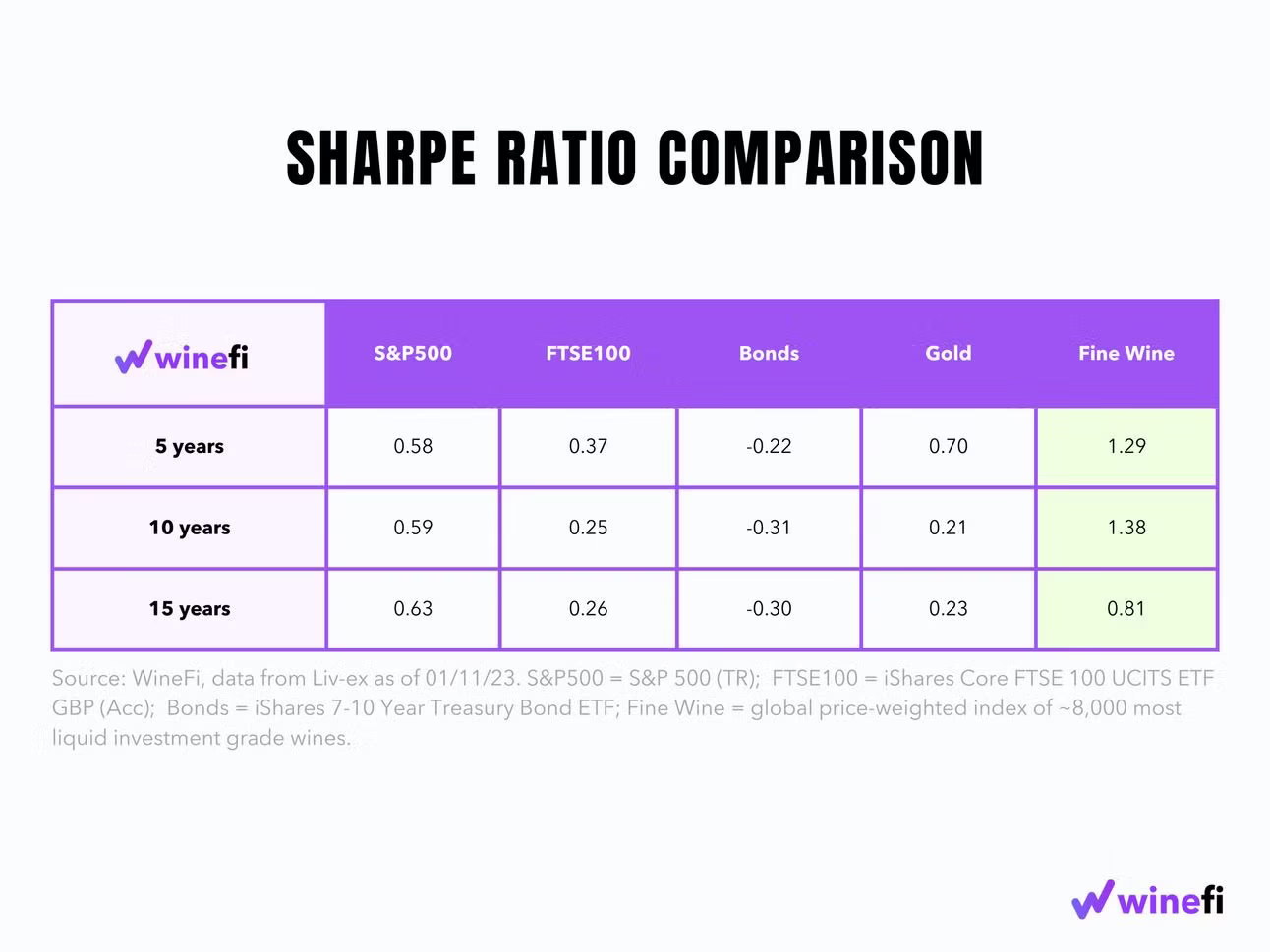

As a result, wine exhibits favourable risk-adjusted returns compared to other asset classes. This is demonstrated by a higher Sharpe Ratio (shown above), which is a measure of the average return of an asset in excess of the risk-free rate and relative to its volatility.

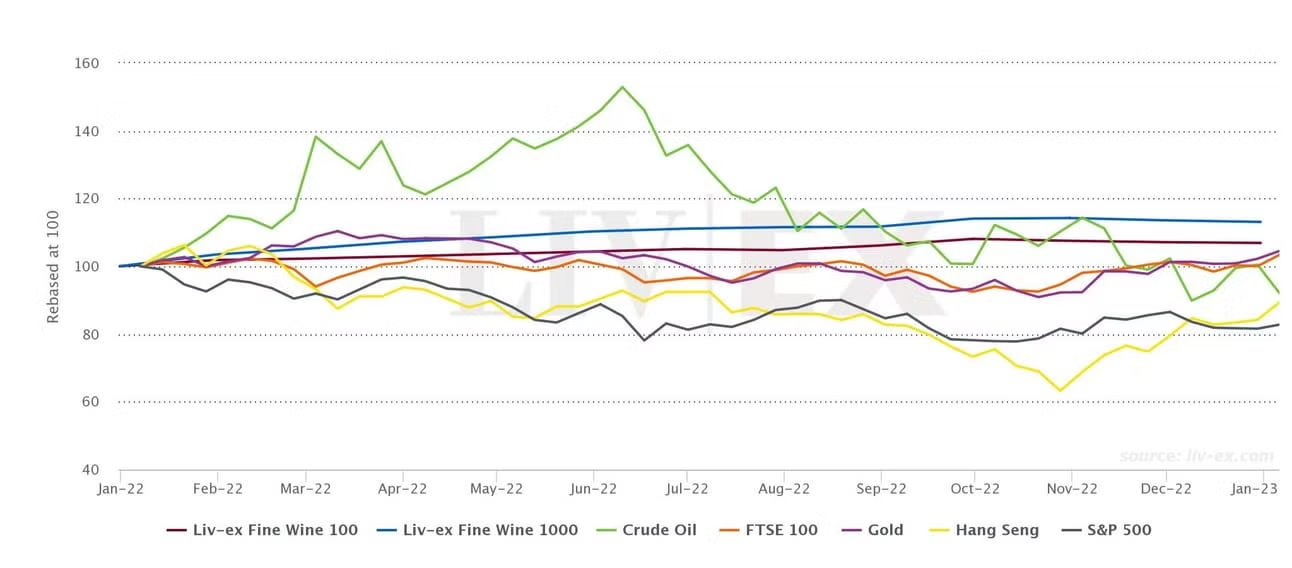

Downside Protection

Source: The Liv-ex

As a tangible asset, wine behaves in a similar manner to gold as a “safe haven” asset. The below chart shows the Liv-ex 100 and Liv-ex 1000 vs. other asset classes.

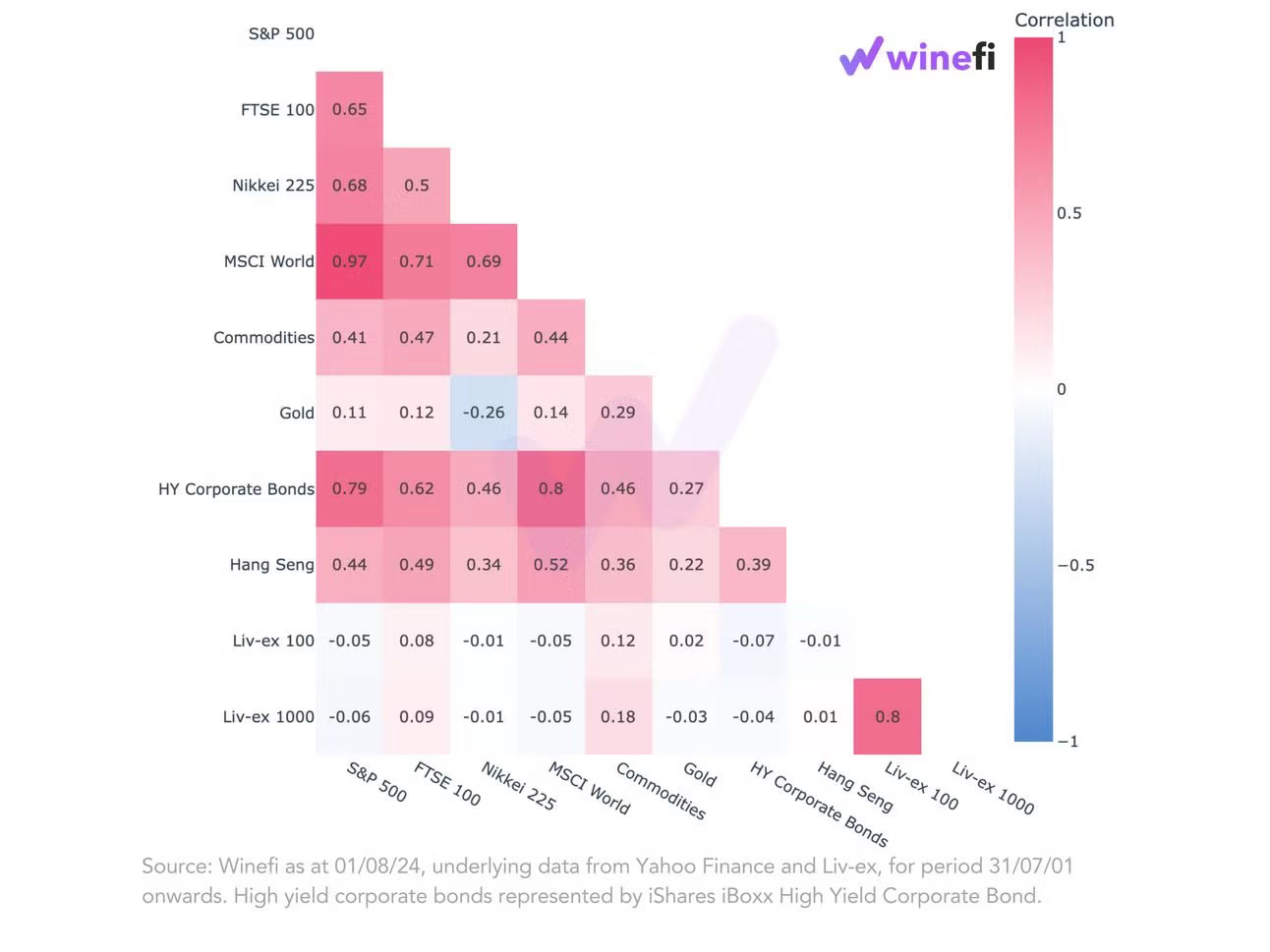

Diversification

Fine wine shows little correlation to other asset classes, making it a useful portfolio diversifier.

The chart above shows the correlation between the Liv-ex 100 and 1000, regarded as the broadest measure of investment-grade wine, and various other indices and markets.

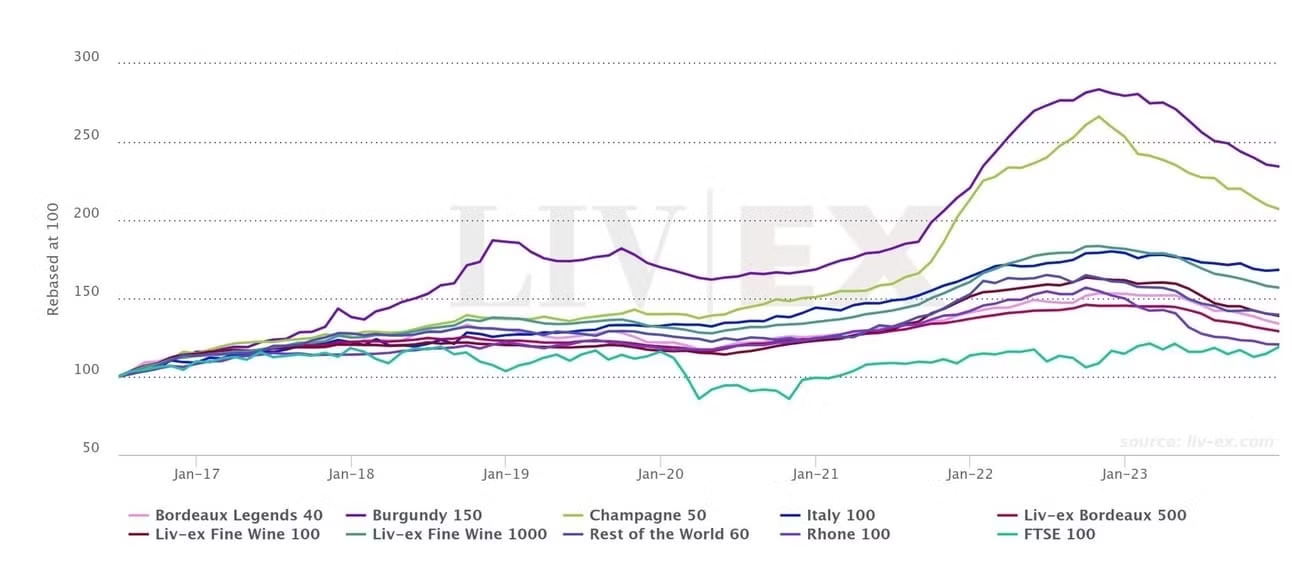

Another facet of fine wine vs. other commodities like oil or gold, is that regional indices perform very differently to one another. The graph below highlights the opportunity for further diversification within wine as an asset class on a regional basis.

Source: Liv-ex

Tax Advantages

It is often claimed that returns made from wine investments are exempt from Capital Gains Tax (CGT). The truth, as always, is more nuanced.

In many cases, wine is regarded by HMRC as a “wasting asset”. Wasting assets are regarded as those with a useful life of less than 50 years.

In these circumstances, no capital gains tax is payable. This carries through to assets held within a shared ownership structure.

Upon investing with WineFi, we will provide you with a Letter of Recommendation from a Specialist Tax Consultant.

When you invest in wine through WineFi, you are buying wine held “in bond”. Wines held in this manner are deemed not to have passed through customs, which means that VAT and Duty is suspended.

Unless these wines are removed from bond, no VAT or Duty are payable on your investment.

Interested in learning more? Click here to speak to one of our team, today.

The Issues

Illiquid

Wine is, ironically, an illiquid asset class. Whilst there are advantages to this (see “Volatility”), it means that wine is a long term investment.

Our relationship with Jera, a Coterie Holdings company, allows you to borrow against the value of your wine collection. This allows you to monetise an otherwise non-yielding portfolio, for the very first time.

We are currently exploring mechanisms that will allow our investors to trade in and out of the wine markets as easy as easily as placing a trade on Robin Hood or eToro.

Hold Period and Storage Costs

Fine Wine is a medium to long-term hold. We typically recommend a hold period of 3-7 years depending on market conditions. This extended timeframe allows for the wine to mature and potentially increase in value, while also providing a buffer against short-term market fluctuations.

It’s important to note that proper bonded storage during this period is crucial to maintain the wine’s quality and provenance. While fine wine can offer attractive returns, investors should be prepared for the costs associated with storage and insurance.

We include the cost of storage and insurance as part of our 10% up front fee, our partnership with Coterie Vaults allows us to pass on discounted storage costs to our customers.

Complex

It is no secret that wine investment is a specialist topic. Many investors who are otherwise knowledgeable about mainstream asset classes may know very little about wine.

As a result, less knowledgeable investors sometimes end up with portfolios filled with wines that are unlikely to appreciate or for which there is no secondary market at all.

Our job is to simplify the experience of investing in wine. We combine in depth data analysis with qualitative analysis from our Investment Committee, and make all research available to the customer, so they are able to make an informed decision.

Capital is at risk. Wine values can go down as well as up, and investments may not perform as expected. Returns may vary. You should not invest more than you can afford to lose. WineFi is not authorised by the Financial Conduct Authority. Investments are not regulated and you will have no access to the Financial Services Compensation Scheme (FSCS) or the Financial Ombudsman Service (FOS). Past performance and forecasts are not reliable indicators of future results and should not be relied on. Forecasts are based on WineFi’s own internal calculations and opinions and may change. Investments are illiquid. Once invested, you are committed for the full term. Tax treatment depends on individual circumstances and may change.

You are advised to obtain appropriate tax or investment advice where necessary.

WineFi is a trading name of WineFi Management Limited. Registered in England and Wales with registration number: 14864655 and whose registered office is at 5th Floor, 167-169 Great Portland Street, London, United Kingdom, W1W 5PF.