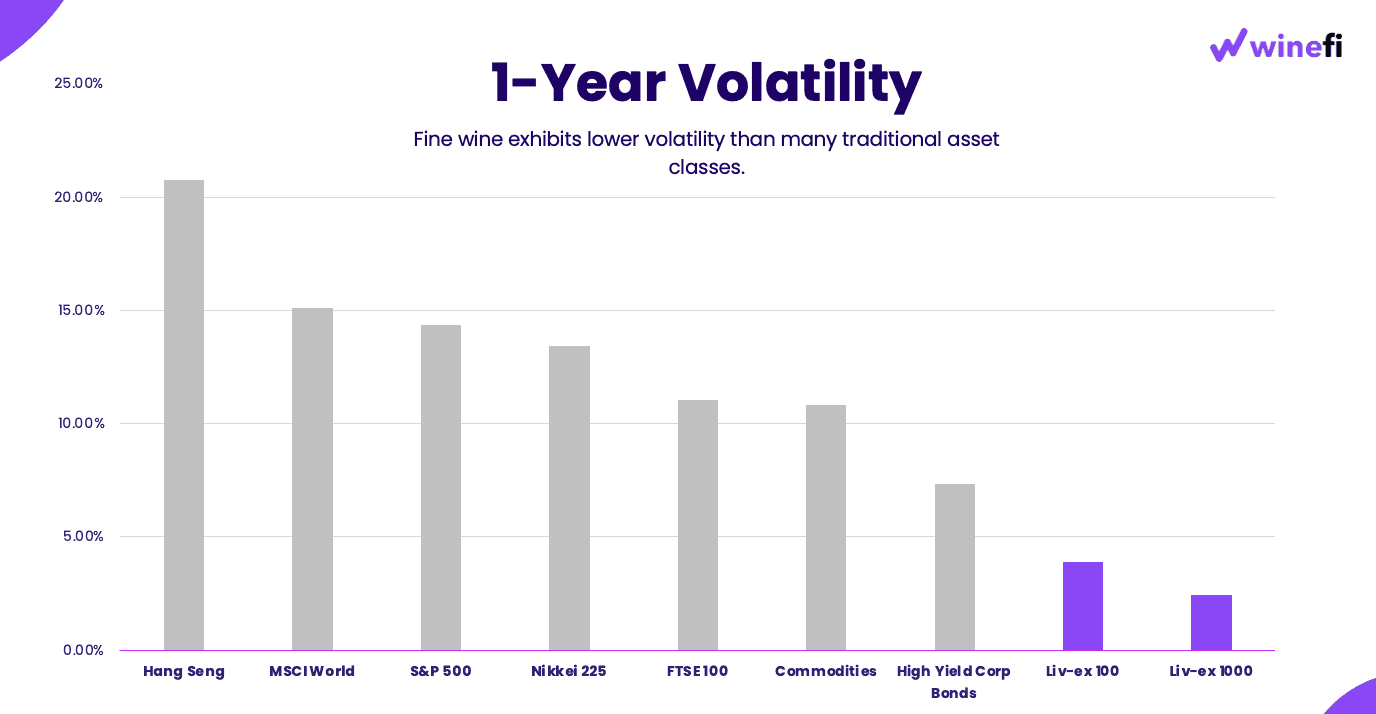

Volatility can be fairly simply defined as the variance of a data set around its mean. The classic Capital Asset Pricing Model (CAPM) view is that returns are a positive and linear function of beta, or volatility. The higher the volatility, the higher the predicted returns.

Source:Underlying data from investing.com, Liv-ex as of 01/01/2024. Liv-ex indices data can be found at https://www.liv-ex.com/news-insights/indices/

There is however a pool of research suggesting that this isn’t the case. Pim Van Vliet, PhD grouped portfolios by volatility in his book “High Returns from Low Risk: A Remarkable Stock Market Paradox” and found that the portfolio with the lowest volatility outperformed that with the highest.

Why is this? There are a few reasons, but for us at WineFi the most compelling is that we as humans are risk averse. We dislike losing more than we like winning. This leads to higher demand for assets where the risk of losing is lower.

As with all things, there is more nuance than we’re able to fit in a short blog post… the point we’re trying to make is that low volatility doesn’t necessarily mean low returns.

Sources: Sources (Liv-ex, Pim van Vliet, PhD, and this excellent Wikipedia page)

Capital is at risk. Wine values can go down as well as up, and investments may not perform as expected. Returns may vary. You should not invest more than you can afford to lose. WineFi is not authorised by the Financial Conduct Authority. Investments are not regulated and you will have no access to the Financial Services Compensation Scheme (FSCS) or the Financial Ombudsman Service (FOS). Past performance and forecasts are not reliable indicators of future results and should not be relied on. Forecasts are based on WineFi’s own internal calculations and opinions and may change. Investments are illiquid. Once invested, you are committed for the full term. Tax treatment depends on individual circumstances and may change.

You are advised to obtain appropriate tax or investment advice where necessary.

WineFi is a trading name of WineFi Management Limited. Registered in England and Wales with registration number: 14864655 and whose registered office is at 5th Floor, 167-169 Great Portland Street, London, United Kingdom, W1W 5PF.