How Much Capital Do You Need for an Optimally Balanced Wine Investment Portfolio?

WineFi Data Team | Portfolio Construction & Strategy

One of the most frequently asked questions we receive from prospective investors is deceptively simple: how much do I need to invest in fine wine? The answer, as with most questions in portfolio management, is that it depends - specifically, on the degree of diversification one wishes to achieve across regions, producers, vintages, and price brackets.

Our data team has conducted extensive analysis of historical pricing data to model optimally diversified portfolios at three capital thresholds: £25,000, £100,000, and £310,000. The findings reveal that while fine wine investing is accessible at lower entry points, the quality of diversification - and with it, the risk-adjusted return profile - improves materially as portfolio size increases.

The Case for Diversification in Fine Wine

Fine wine is not a monolithic asset class. Regional performance leadership rotates over time: Bordeaux dominated returns from 2003 to 2011, only to stagnate thereafter. Burgundy and Tuscany have since emerged as the strongest performers. Champagne occupies an interesting middle ground, delivering returns closer to Burgundy in magnitude but with the consistency more typically associated with Tuscany.

This rotation is precisely why regional diversification matters. A portfolio concentrated in a single region - however strong its recent track record - carries the risk of regime change. Our analysis of the past twenty years of pricing data demonstrates that no single region has sustained dominance for more than a decade.

Price diversification is equally important. Over the past seven years, wines priced below £9,600 per twelve-bottle case have produced a higher proportion of exceptional performers (those averaging compound annual growth rates above 25%) than wines priced above that threshold. These breakout wines are often producers newly entering the mainstream investment-grade consciousness - names such as Domaine Arnoux-Lachaux, whose wines appreciated tenfold over a short period.

However, the most consistently strong and predictable returns have historically been found in the £9,600 to £19,200 range, where established names such as Domaine de la Romanée-Conti (DRC) reside. These wines are unlikely to deliver explosive short-term gains, but they have demonstrated remarkably stable appreciation across virtually all vintages.

Portfolio Tier 1: £25,000

At this capital level, meaningful constraints emerge. A portfolio of this size can typically accommodate four regions, with two to five producers per region and only a single vintage per label. The investor is limited to smaller case sizes and individual bottles, and there is no capacity for vintage diversification within a given label without sacrificing breadth elsewhere.

Critically, a £25,000 portfolio cannot access the optimal price bracket (£9,600-£19,200 per case) without committing an outsized proportion of capital to a single position. This concentration risk is the primary limitation at this tier.

Portfolio Tier 2: £100,000

At £100,000, the portfolio begins to resemble what our models identify as a structurally sound allocation. Seven regions can be covered in meaningful proportions. Label diversification improves to three to nine producers per region, and larger case sizes - which tend to be a better store of value and command a premium on the secondary market - become accessible.

The principal trade-off at this level is between label diversification and vintage diversification. Portfolio construction requires deliberate choices between holding multiple vintages of a strong label versus a single vintage across multiple strong labels. A modest allocation to the highest-value blue-chip wines is achievable, though smaller than would be ideal.

Portfolio Tier 3: £310,000

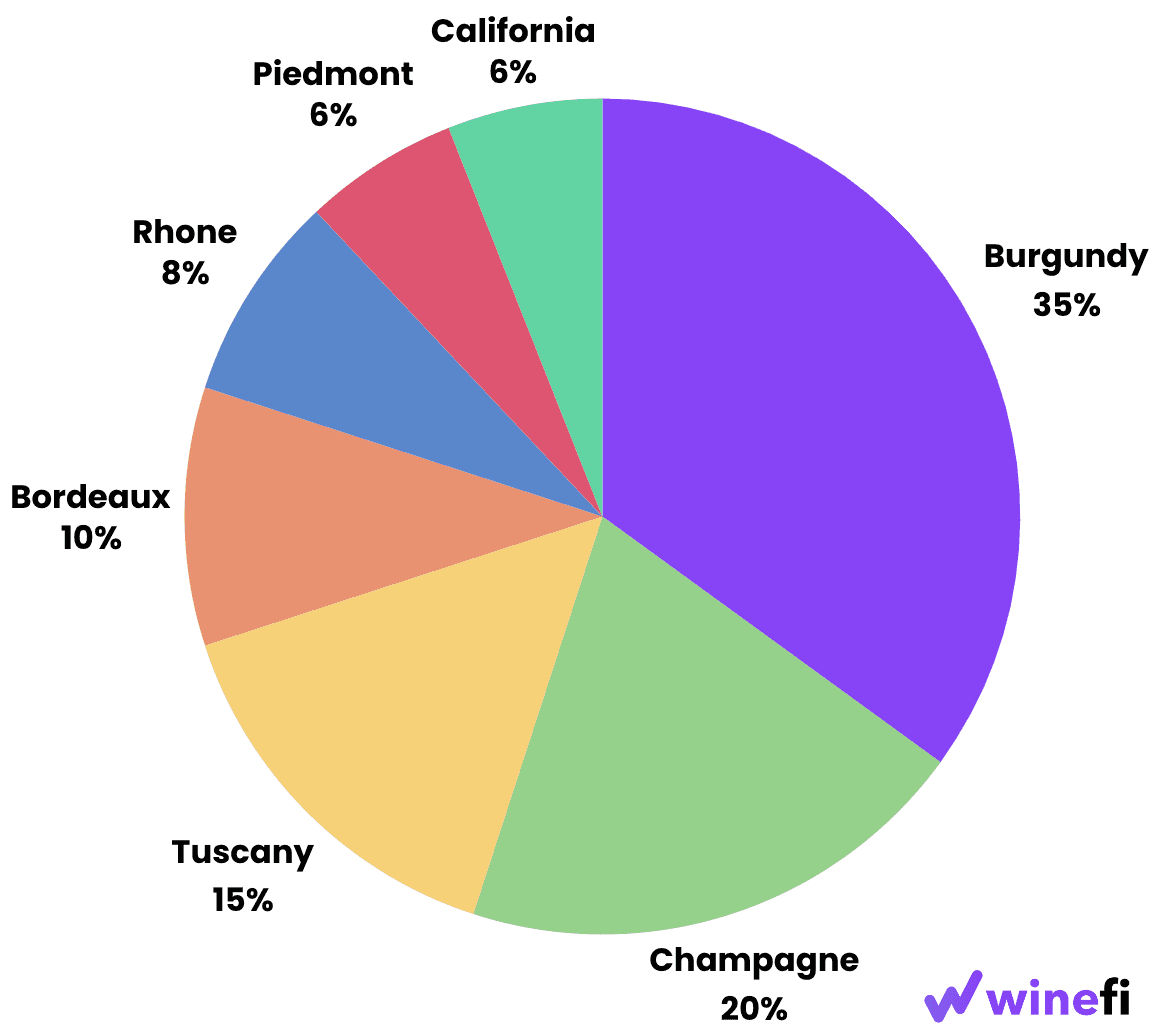

This threshold represents what our modelling identifies as the point at which an investor can construct a truly optimally balanced portfolio. All seven major investment-grade regions are covered in proportions our analysis suggests are optimal for achieving an historic annualised compound growth rate of approximately 13.5%. Label diversification extends to five to fifteen labels per region, including multiple labels from a single producer where appropriate (for instance, multiple cuvées from DRC or Leroy in Burgundy). Vintage diversification - one to three vintages per label - manages the risk of any single vintage underperforming. And the inclusion of larger and rarer case formats provides additional upside potential through scarcity premiums.

Beyond £310,000

Capital above this threshold unlocks further advantages: meaningful allocation to emerging European investment regions such as Loire, Rioja, and Mosel; exposure to New World regions including South Africa and South Australia; greater vintage diversification within individual labels; and access to truly collectible items - older Bordeaux and Burgundy that have passed their drinking windows but retain (and often appreciate in) value as rarities.

Our Optimal Allocation

Based on analysis of returns across all liquid investment-grade wines over multiple look-back periods, our current recommended portfolio composition targets the following:

Optimal price brackets by look-back period:

Look-back Period | Optimal Price Range (12×75cl Case) |

|---|---|

5 years | £15,600 - £18,000 |

7 years | £13,200 - £18,000 |

10 years | £8,400 - £13,200 |

Returns by price bracket (all liquid investment-grade wines):

Price Range (£) | Avg. 7yr CAGR (%) | Avg. Lifetime CAGR (%) | Cross-Vintage Std Dev (%) |

|---|---|---|---|

9,601-19,200 | 13.61 | 13.99 | 7.14 |

19,201+ | 11.48 | 12.90 | 7.51 |

4,801-9,600 | 10.08 | 10.69 | 9.43 |

2,401-4,800 | 8.31 | 8.68 | 8.35 |

1,201-2,400 | 8.01 | 8.22 | 7.80 |

1,200 and less | 7.15 | 6.79 | 7.34 |

The data is clear: the £9,600-£19,200 bracket has historically delivered the highest average returns with the lowest cross-vintage volatility - the best risk-adjusted performance in the investment-grade universe.

The WineFi Approach

Our proprietary WineFi Investment Score (WIS) is built on over twenty-five years of pricing data and evaluates historical price trends, critic scores, brand reputation, vintage quality, and market conditions to identify wines that are currently undervalued and most likely to outperform. We would expect a diversified portfolio of £200,000 to £400,000 to achieve approximately 12% compound annual growth over a five-to-seven-year investment horizon.

For investors unable to commit capital at the higher thresholds, our syndicate structure provides access to the diversification benefits of a larger portfolio from as little as £3,000 - enabling individual investors to gain exposure to the optimal regional and price composition that would otherwise require substantially more capital.

Capital is at risk. Wine values can go down as well as up, and investments may not perform as expected. Returns may vary. You should not invest more than you can afford to lose. WineFi is not authorised by the Financial Conduct Authority. Investments are not regulated and you will have no access to the Financial Services Compensation Scheme (FSCS) or the Financial Ombudsman Service (FOS). Past performance and forecasts are not reliable indicators of future results and should not be relied on. Forecasts are based on WineFi’s own internal calculations and opinions and may change. Investments are illiquid. Once invested, you are committed for the full term. Tax treatment depends on individual circumstances and may change.

You are advised to obtain appropriate tax or investment advice where necessary.

WineFi is a trading name of WineFi Management Limited. Registered in England and Wales with registration number: 14864655 and whose registered office is at 5th Floor, 167-169 Great Portland Street, London, United Kingdom, W1W 5PF.